For years, a dangerous myth has circulated in the crypto world: that blockchain technology is the ultimate tool for hiding money from governments. The idea is seductive. You send Bitcoin or Ethereum across borders without asking permission, bypassing traditional banks and their red tape. But here is the hard truth that regulators have been shouting from the rooftops since 2022: cryptocurrency is not anonymous, and trying to use it to evade financial sanctions is one of the riskiest legal moves you can make.

If you are considering using digital assets to bypass restrictions imposed by entities like the U.S. Department of the Treasury’s Office of Foreign Assets Control (OFAC), you need to understand that the regulatory net has tightened dramatically. What was once seen as a gray area is now a bright red line with severe criminal consequences. This analysis breaks down why circumventing crypto restrictions is legally perilous, technically traceable, and increasingly futile.

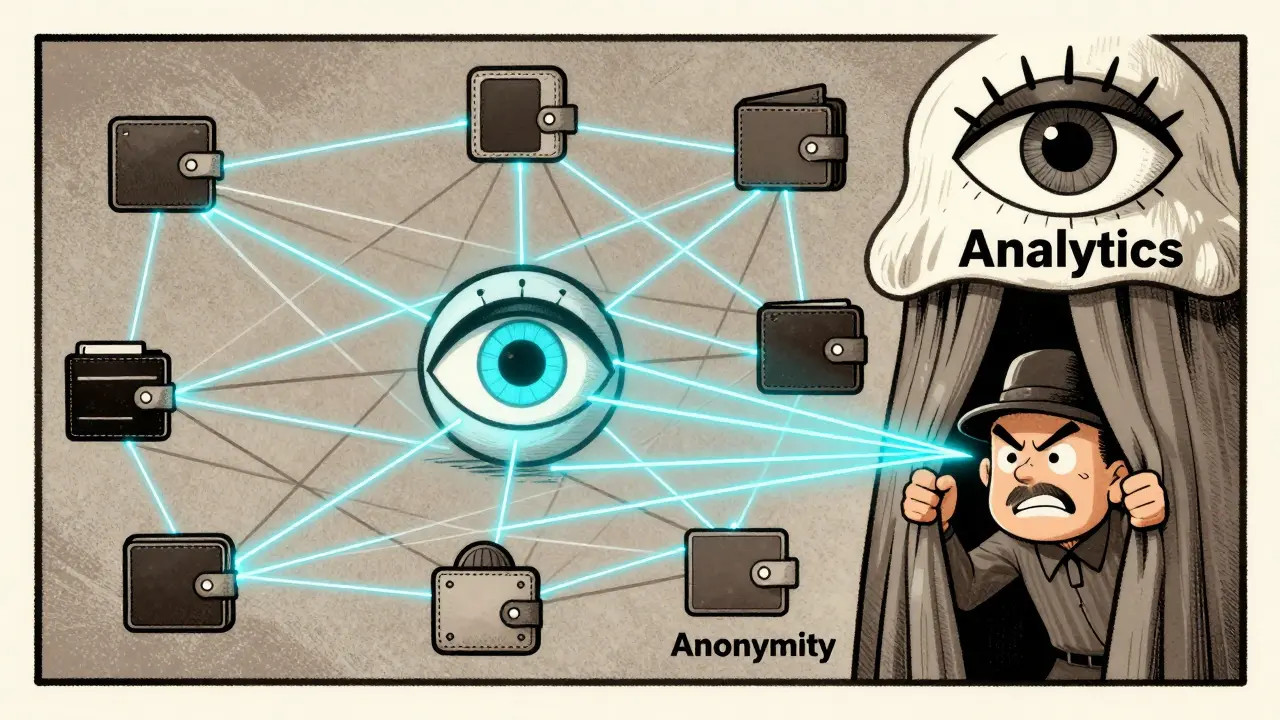

The Myth of Anonymity vs. The Reality of Traceability

The biggest misconception fueling sanctions evasion attempts is the belief that cryptocurrencies offer true anonymity. In reality, most major blockchains are pseudonymous at best. Every transaction is recorded on an immutable public ledger. While your name isn’t directly attached to your wallet address, the transaction history is permanent and visible to anyone who knows how to look.

This transparency is the enemy of evasion. According to the Financial Action Task Force (FATF), virtual assets are far from anonymous. Director David Lewis stated clearly in June 2022 that blockchain analytics tools allow authorities to monitor these transactions effectively. The data backs this up. Reports from Chainalysis in 2023 revealed that blockchain analytics firms can trace approximately 98% of transactions on major networks like Bitcoin and Ethereum. Even privacy-focused coins like Monero, which were thought to be safer havens, showed only 65% traceability-a number that continues to drop as forensic techniques improve.

When you attempt to move funds through a sanctioned channel, you aren't disappearing into the ether. You are leaving a digital paper trail that is often more permanent than records in traditional banking systems, where data might be purged after certain retention periods. This permanence makes it easier for law enforcement to build cases long after the transaction occurs.

Global Regulatory Frameworks Are Closing Loopholes

Governments worldwide have realized that if they want sanctions to work, they must regulate crypto. The days of the "wild west" are over. Major jurisdictions have implemented strict frameworks that apply equally to digital assets and traditional finance.

| Jurisdiction/Body | Key Regulation/Guidance | Impact on Evasion Attempts |

|---|---|---|

| United States (OFAC) | Sanctions Compliance Guidance for Virtual Currency (Oct 2021) | Made sanctions evasion using crypto a clear criminal offense; maintains a list of blocked wallet addresses. |

| European Union | Markets in Crypto-Assets Regulation (MiCA) (Apr 2023) | Mandates transaction monitoring systems for service providers to identify sanctioned entities. |

| United Kingdom (FCA) | Joint Statement with Bank of England (Mar 2022) | Explicitly requires all UK financial services, including crypto, to comply with sanctions. |

| New York (NYDFS) | BitLicense & Enforcement Actions | Strict licensing requirements; active prosecution of non-compliant entities. |

In the United States, OFAC published specific guidance in October 2021, establishing formal expectations for the industry. As of December 2023, the Specially Designated Nationals and Blocked Persons List (SDN) contained 1,571 specific crypto wallet addresses. Transacting with any of these addresses is illegal. The EU’s MiCA regulation, adopted in April 2023, goes further by requiring crypto-asset service providers to implement screening protocols that meet FATF standards by December 2024. This means exchanges and custodians are legally obligated to flag and freeze funds associated with sanctioned individuals or regions.

The message from regulators is consistent: there is no exemption for digital assets. The Financial Conduct Authority (FCA) in the UK and the European Commission have made it clear that financial sanctions regulations apply to crypto just as they do to dollars or euros. Ignorance of these rules is not a defense in court.

Why Crypto Is Actually Worse Than Cash for Evasion

You might think that sending crypto is harder to track than smuggling physical cash. The data suggests otherwise. A 2023 report by the Center for Strategic and International Studies (CSIS) analyzed $148 billion in estimated sanctions evasion attempts related to Russia as of September 2023. Surprisingly, cryptocurrency represented only 0.01% of that volume.

Traditional methods dominated: commodity trading accounted for 42%, third-country intermediaries for 38%, and physical cash smuggling for 15%. Why is crypto so rare? Because it leaves a footprint. When you use a centralized exchange-which handles the vast majority of retail volume-you are subject to Know Your Customer (KYC) checks. Exchanges like Coinbase and Binance have demonstrated aggressive compliance. Within 48 hours of the February 2022 invasion of Ukraine, Coinbase froze 25,000 Russian accounts holding roughly $225 million. Binance implemented proof-of-address verification for Russian users with significant holdings shortly after.

Furthermore, the volatility of crypto adds risk. During the first three months of 2022, frozen Russian crypto assets fluctuated by 35% in value. If you are trying to move value out of a restricted zone, you risk losing a significant portion of its worth before you even complete the transfer. Traditional banking channels, while heavily monitored, offer stability. Crypto offers neither anonymity nor stability for those trying to break the law.

The Role of Blockchain Analytics Firms

The rise of specialized blockchain analytics companies has been the death knell for easy crypto evasion. Firms like Chainalysis, Elliptic, and TRM Labs sell their software to governments and financial institutions. These tools cluster wallet addresses, link them to real-world identities, and flag suspicious patterns in real-time.

In 2023, these firms reported a 99.2% detection rate for transactions involving sanctioned Russian entities, up from 87% in 2021. They look for specific "red flags" established by the U.S. Treasury’s Financial Crimes Enforcement Network (FinCEN). These include:

- Transactions initiated from IP addresses in jurisdictions known for weak sanctions enforcement.

- Transfers to wallets previously identified on the OFAC SDN list.

- Usage of decentralized exchanges (DEXs) located in high-risk jurisdictions.

- Rapid movement of funds through multiple "mixer" services to obscure origins.

Professor Aaron Wright of Cardozo Law School noted in the Harvard International Law Journal that this creates a "digital paper trail that is far more permanent and traceable than traditional financial transactions." Even if you use a peer-to-peer platform, the moment you try to convert that crypto back into fiat currency or spend it on regulated goods, you hit a compliance wall. The ecosystem is designed to catch outliers.

Legal Consequences and Criminal Prosecutions

The stakes have never been higher. Regulators are moving beyond fines and into criminal prosecutions. The U.S. Department of Justice’s Cryptocurrency Enforcement Framework, published in October 2020, explicitly warned that virtual currencies undermine financial markets and harm national interests. This wasn't just talk.

In November 2023, the DOJ charged two Russian nationals with attempting to evade $1.3 billion in sanctions through cryptocurrency transactions. This marked the first criminal prosecution specifically targeting crypto-based sanctions evasion. The implications are severe: prison time, asset forfeiture, and permanent bans from the financial system.

Corporate actors are not safe either. Nexo Inc. settled with five state coalitions for $22.5 million in January 2023 after being accused of offering unregistered securities and failing to maintain adequate compliance controls. Nine states, including California and New York, filed coordinated enforcement actions against Coinbase in June 2023. These cases signal that regulators will hold both individuals and platforms accountable.

If you are a business owner, implementing compliance is expensive but necessary. Coinbase’s transparency report from March 2023 revealed that building robust compliance infrastructure took 18 months and cost $47 million initially, with ongoing quarterly costs of $12.3 million. However, the alternative-facing federal indictment-is infinitely more costly.

Future Outlook: Decentralized Finance and Privacy Tech

As centralized exchanges tighten their grip, some evaders turn to Decentralized Finance (DeFi) protocols and privacy-enhancing technologies. However, regulators are already pivoting to target these areas. Dr. Marius Janson of Norton Rose Fulbright predicted in January 2024 that the next frontier of enforcement will focus on DeFi protocols.

The proposed Digital Asset Sanctions Compliance Act, introduced in the U.S. Congress in September 2023, aims to extend sanctions requirements to decentralized applications. The goal is to ensure that even code cannot be used to bypass international law. Meanwhile, the FATF projects that traceability for major cryptocurrencies will reach 99.8% by 2026 through coordinated international efforts.

While privacy coins like Monero present challenges, their adoption remains limited due to delisting from major exchanges and increased scrutiny. The window for using crypto as a viable sanctions evasion tool is closing rapidly. The combination of advanced analytics, strict global regulations, and aggressive enforcement makes it a high-risk, low-reward strategy.

Is it illegal to use cryptocurrency if I live in a sanctioned country?

It depends on the specific sanctions. Generally, owning crypto is not illegal, but transacting with blocked persons or entities is. For example, U.S. citizens cannot buy crypto from sanctioned countries, and residents of sanctioned countries cannot access U.S.-based exchanges. Attempting to bypass these blocks via mixing services or foreign exchanges can lead to criminal charges for sanctions evasion under laws enforced by OFAC.

Can blockchain analytics really trace my transactions?

Yes, for most major cryptocurrencies like Bitcoin and Ethereum. Analytics firms use clustering algorithms to link wallet addresses to real-world identities based on KYC data from exchanges, IP logs, and spending patterns. As of 2023, they can trace approximately 98% of transactions on these networks. Only privacy-focused coins offer more resistance, but even those are becoming less effective against advanced forensic tools.

What happens if I accidentally send crypto to a sanctioned wallet?

You must immediately cease all further transactions and report the incident to the relevant regulatory body, such as OFAC in the U.S. Failure to report can be seen as complicity. Depending on the jurisdiction and the nature of the error, you may face penalties, though voluntary disclosure often mitigates punishment. Do not attempt to "fix" it by moving the funds further, as this increases suspicion.

Are decentralized exchanges (DEXs) safe from sanctions enforcement?

Not necessarily. While DEXs do not require KYC, regulators are developing ways to sanction the developers, liquidity providers, or front-end interfaces of these protocols. Additionally, if you ever bridge your assets back to a centralized exchange or withdraw to a fiat bank account, the transaction will be screened. Using a DEX does not erase the transaction history on the blockchain, which remains visible to analysts.

How does the EU's MiCA regulation affect crypto sanctions?

MiCA requires all crypto-asset service providers operating in the EU to implement robust sanctions screening protocols. By December 2024, these providers must meet FATF standards, meaning they must actively monitor transactions for links to sanctioned entities. This creates a unified, strict compliance environment across Europe, reducing opportunities for regulatory arbitrage within the region.

Kenneth Riley

June 14, 2026 AT 00:26the whole premise is flawed because they are watching everything anyway so why bother trying to hide it if you are already caught

its not about anonymity its about control and they have won that game long ago

people still think mixing coins works but chainalysis just flags the mixer itself as a sanctioned entity now so you are painting a target on your back by using them

Akeem Whittaker

June 14, 2026 AT 08:06You make some valid points about the traceability of major chains like Bitcoin, but we need to be careful not to generalize this to all decentralized finance protocols. While centralized exchanges are indeed under heavy scrutiny, the architecture of true DeFi allows for permissionless interaction that regulators struggle to pin down. The key distinction lies in whether there is a central point of failure or control. If no single entity controls the protocol, can it truly be sanctioned? This is where the legal theory gets murky and interesting for us.

Abby Sivertsen

June 14, 2026 AT 21:02I feel like people forget how much pressure is actually put on these platforms when things go south

it is scary to think about how quickly they freeze accounts without even asking questions sometimes

we treat crypto like digital cash but it acts more like a tracked credit card with extra steps

Benjamin Eisen

June 15, 2026 AT 12:39i think the part about volatility is really important here and often overlooked by those trying to move money out quickly

if you are trying to evade sanctions you are also exposed to market risk which can wipe out half your value before you even get to the off ramp

plus the kyc checks are getting tighter every day so its not worth the hassle honestly

ravi mahla

June 17, 2026 AT 06:16Haha, yeah, good luck hiding from the IRS with a blockchain ledger that never forgets anything

It is funny how people still believe in the wild west narrative when the cops have been patrolling the streets since 2021

Just use a bank account and pay your taxes like a normal person instead of playing detective with mixers

Mark Brunschwiler

June 17, 2026 AT 19:47The soul of freedom dies when we accept surveillance as the price for participation in the global economy

We are building a cage of our own making and calling it security while the walls close in tighter every day

Why do we keep feeding the beast when it only grows hungrier for our data and our liberty

Sonya O'Brien

June 19, 2026 AT 19:35I completely agree with the assessment regarding the EU's MiCA regulation because it creates a unified front that eliminates the regulatory arbitrage opportunities that existed previously across different member states. When you consider that service providers must now implement screening protocols that meet FATF standards by December 2024, it becomes clear that the window for casual non-compliance is shutting rapidly. It is not just about the technology anymore; it is about the legal obligations placed on the intermediaries who facilitate the entry and exit of funds into the traditional financial system. This collaborative approach among European nations sets a precedent that other jurisdictions are likely to follow, thereby creating a global net that is increasingly difficult to escape.

Filbert Reeves

June 20, 2026 AT 16:06they want you to believe that the blockchain is transparent but what about the dark pools and the private transactions that never hit the public ledger

the government has been manipulating the markets for decades and now they are trying to take away the one tool that could give power back to the people

trust me when i say that the real evasion happens in the shadows where their eyes cannot see and they are terrified of losing control over that space

keep digging deeper and you will find that the entire system is rigged against the individual from the start

Nick Rice

June 21, 2026 AT 19:30Let us look at the facts here. The DOJ charging two Russian nationals for $1.3 billion in sanctions evasion is not a theoretical threat. It is a concrete example of the consequences. If you are thinking about testing the waters, stop right now. The infrastructure for compliance is robust, expensive, and legally binding. There is no gray area left. You either comply or you face criminal prosecution. Simple as that.

Amit Thakur

June 21, 2026 AT 20:07The integration of AI-driven clustering algorithms by firms like Chainalysis and Elliptic has fundamentally altered the threat landscape for illicit actors. We are seeing a paradigm shift where heuristic analysis can link pseudonymous addresses to real-world identities with unprecedented accuracy. The 99.2% detection rate for sanctioned entities is not a static number; it is an accelerating trend driven by machine learning models that continuously improve their pattern recognition capabilities. For any entity operating in the virtual asset space, ignoring these technological advancements is akin to professional suicide.

Eric Scheinberg

June 22, 2026 AT 05:18The legal framework is unequivocal. OFAC guidance is clear. Compliance is mandatory. Failure to adhere results in severe penalties. One must understand the gravity of transacting with blocked persons. The SDN list is comprehensive. Ignorance is not a defense. Proceed with caution and strict adherence to regulations.

pankaj chawla

June 23, 2026 AT 05:03This is a very well-researched article and I appreciate the detailed breakdown of the regulatory bodies involved. It is crucial for everyone in the industry to stay updated on these changes especially with MiCA coming into full effect soon. Collaboration between regulators and tech companies seems to be the only way forward to ensure integrity in the market.

Jessica Lane

June 24, 2026 AT 00:27I am curious about the specific impact on small businesses that may not have the resources to implement such expensive compliance infrastructure. While large players like Coinbase can afford millions in compliance costs, smaller entities might struggle to keep up. Does this create a barrier to entry that favors established corporations over innovative startups?

Charles Pawlikowski

June 25, 2026 AT 12:55about time someone said it loud and clear :crypto is for criminals and terrorists and we need to shut it down completely

these people are trying to destroy our national security by bypassing sanctions that protect our values

ban it all and let the bad guys starve :)

Andrea Burd

June 26, 2026 AT 14:42another boring article about rules nobody wants to read

like anyone actually cares about ofac guidelines when they can just buy monero and disappear

typical establishment propaganda designed to scare ordinary people into submission

Manish Prajapat

June 26, 2026 AT 19:17The philosophical implication here is profound. We are witnessing the end of privacy as a fundamental human right in the digital age. The blockchain was promised as a tool for liberation, yet it has become the ultimate instrument of surveillance. Perhaps the true lesson is not about how to evade sanctions, but about the necessity of rethinking our relationship with state authority and financial systems altogether. Is there a path forward that respects both security and individual autonomy?